{kind=link}

Golden Rules of Accounting – Every economic entity must provide financial information to all of its stakeholders. The financial information provided must be accurate and present a true picture of the entity. It must account for all of its transactions for this presentation.

Accounting must be consistent because economic entities are compared to understand their financial status. There are three Golden Rules of Accounting that must be followed to achieve uniformity and correctly account for transactions. These rules serve as the foundation for entering journal entries, which serve as the foundation for accounting and bookkeeping.

Table of Contents

Types of Accounts

To comprehend the Golden Rules of Accounting, we must first understand the various types of accounts. The account classification applies to all general ledger types. In other words, each account will fall into one of the broad categories listed below. Reserves are classified into three types:

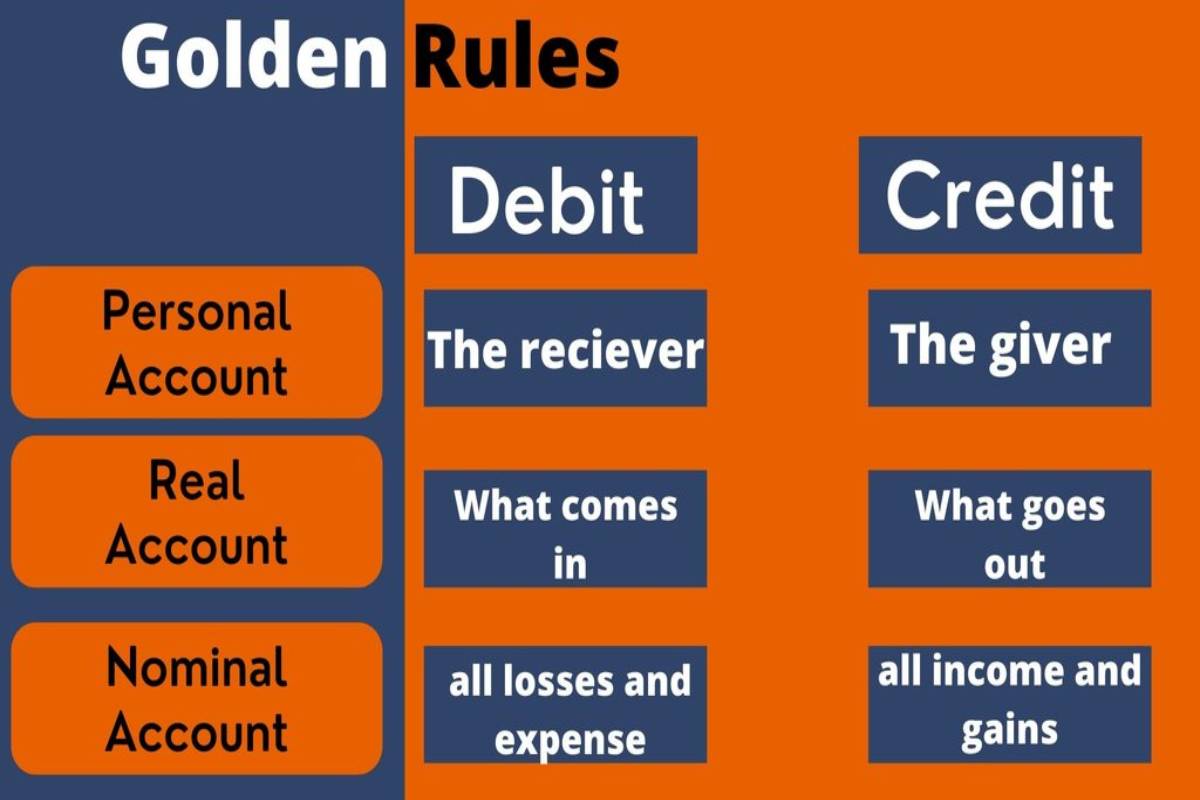

Real Account

A Real Account is a general ledger account that deals with assets and liabilities other than people accounts. These accounts do not close at the end of the fiscal year and are carried forward. A bank account is an example of a Real Account.

Personal Account

A personal account is a General ledger account link to all people, including individuals, businesses, and organizations. A Creditor Account is an example of a Personal Account.

Nominal Account

A Nominal account is a General ledger account that records all income, expenses, losses, and gains. An Interest Account is an example of a Nominal Account.

3 Golden Rules of Accounting

The basic rules of accounting are as follows:

- Real Account: Debit what comes into the business, Credit what goes out from the business

- Personal Account: Debit the Receiver, Credit the giver

- Nominal Account: Debit the expense or loss of the company; Credit means income or gain of the business

Accounting rules take been develope base on the nature of all accounts. There is a set of Golden Rules for each account, so there are three Golden Rules of Accounting. The Golden Rules define how all transactions in the business are handle.

Conclusion

An entity’s transactions must record. To account for these transactions, the entity must create journal entries, which are then aggregate into ledgers. The journal entries are approve following the accounting Golden Rules. First, determine the type of account to apply these rules, then use these rules.

- Debit what comes in, Credit what goes out

- Debit the Receiver, Credit the giver

- Also Debit all expenses, Credit all incomes

These are known as the Golden Rules of Accounting because they lay the foundation for accounting. They are comparable to the letters of the English alphabet. If a person does not know the letters, he cannot form words and thus cannot use the language. Similarly, if one does not know the golden rules of accounting, he will be unable to pass journal entries and therefore will not account for the transactions accurately. Click here to know about the SBI UPI transaction limit.

Also Read: What are your first-aid responsibilities as an employer?